The Strategy That Saved $15,100 in Tax and Boosted a Retirement by $110k

When it comes to selling an investment property, timing and strategy can make a significant difference to your tax bill. One of our clients recently faced this situation and, through a well-planned approach, we were able to help her save $15,100 in tax, increase her annual tax deductions, and boost her retirement nest egg by over $110,000.

The Situation

Our client, in her late 50s, was preparing to transition into retirement. She owned two investment properties and was considering selling one to clear debt on both. After a conversation with her partner, she decided that reducing debt would provide greater financial security heading into retirement.

Initially, she planned to sell while still earning a full-time salary of $80,000. The property had appreciated in value, and she was set to realise a $100,000 capital gain—but this would have significantly increased her taxable income and triggered a large capital gains tax (CGT) bill.

When she came in to complete her tax return, we took the time to understand her long-term goals—security, more time to travel with her partner, and a smooth transition into retirement. It was through this conversation, part of our Financial Planning Discovery Program, that we proposed a more strategic path forward.

A Strategic Approach

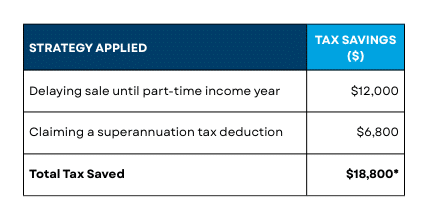

Instead of proceeding with the sale immediately, we advised her to:

Delay the sale until the next financial year, when her income would drop to $40,000 due to part-time work.

→ This alone saved $12,000 in tax.

Repay debt on the sold property only, rather than using all proceeds to clear both loans—freeing up more capital for future investment.

Contribute part of the proceeds to super, creating a tax deduction that offset her remaining CGT.

→ An additional $6,800 in tax saved.

The Financial Impact

*Excludes Medicare levy.

Additionally, through this structure:

- She gained $5,000 in annual tax deductions (from loan interest and our advice fees),

- And improved her net retirement savings by over $110,000 between now and retirement.

Key Takeaways

When selling an investment property, timing matters—especially if your income is about to decrease.

Using superannuation strategically can offset CGT and boost retirement funds.

A clear plan aligned with your personal goals can create better outcomes than a short-term fix.

Get Help Before You Act

If you plan to sell property or other investments, let’s talk about how to make it work best for your circumstances—or explore options that may be even more effective.

General Advice Disclaimer: This article provides general information only. It does not consider your personal circumstances and should not be relied on as taxation or financial advice.