Smash That Debt: The Two Best Ways to Pay It Off

“How am I supposed to save for the fun stuff when my debts are eating up everything I earn?”

If this sounds familiar, you’re not alone. Juggling multiple debts can feel like an endless uphill battle – draining your energy, your wallet, and your ability to plan for the future. But here’s the good news: there is a way out.

Actually, there are two.

Both the Avalanche Method and the Snowball Method work on a simple yet powerful principle: as you clear each debt, the money you were using to repay it is redirected to tackle the next one. This creates a snowball effect, where your repayments grow bigger and bigger over time, helping you crush debt faster.

With a solid strategy, you can take control and start making real progress. Let’s break down these two approaches and explore which one might suit your situation.

Avalanche Method: Tackle High Interest First

The Avalanche Method is all about efficiency. It prioritises paying off the debt with the highest interest rate first while maintaining minimum payments on all other debts. Once the highest-interest debt is cleared, the money that was being directed to that debt is now used to tackle the next highest-interest debt, and so on.

This approach saves you the most money in the long run by minimising the total amount of interest you pay.

Example:

Dave has the following debts:

- Credit card debt of $20,000 at 19% interest

- Personal loan of $10,000 at 10% interest

- Car loan of $75,000 at 7% interest

Using the Avalanche Method, Dave directs as much as possible to paying off the high-interest credit card debt first, while keeping minimum payments on the personal loan and car loan. Once the credit card is cleared, Dave applies the freed-up money to the personal loan, and finally, the car loan.

This method requires patience but delivers substantial savings in interest over time.

When to Choose the Avalanche Method:

- You’re focused on long-term financial savings.

- You want to reduce the amount of interest you’re paying.

- You’re disciplined and don’t mind waiting longer to see results.

Snowball Method: Build Momentum with Quick Wins

The Snowball Method focuses on building momentum. Instead of prioritising by interest rates, you tackle your smallest debt first, regardless of the interest rate, while maintaining minimum payments on the rest. Once the smallest debt is repaid, you redirect that freed-up money to the next smallest debt, and so on.

This method works well for those who need to see quick wins to stay motivated.

Example:

Sarah, a young professional with a growing family, has the following debts:

- Credit card debt of $20,000 at 18% interest

- Car loan of $75,000 at 7% interest

- Mortgage of $750,000 at 6% interest

Using the Snowball Method, Sarah starts by focusing on the $20,000 credit card debt. By repaying this smaller debt quickly, Sarah experiences a sense of achievement that motivates her to tackle the $75,000 car loan next.

Once these smaller debts are cleared, Sarah channels her increased cash flow towards paying down her mortgage faster, putting her on track to achieve her longer-term goals.

When to Choose the Snowball Method:

- You need quick wins to stay motivated.

- You prefer a psychological boost to help you stay committed.

- You find the idea of tackling the largest debts overwhelming.

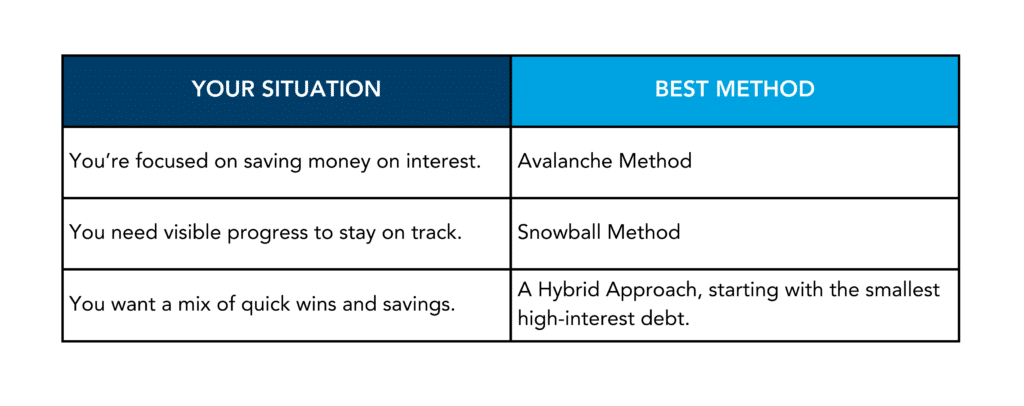

Choosing the Right Method

Your financial situation and personality will influence which method is best for you. Here’s a quick guide:

Debt Strategies for Every Goal

We understand that debt repayment can feel overwhelming. Whether you prefer the precision of the Avalanche Method or the steady motivation of the Snowball Method, we can help you tailor a strategy that works for you.

And if your focus is on reducing your mortgage, we’ve got you covered there too. Strategies like debt recycling can turn your mortgage into a powerful tool for building wealth while you pay it down.

Ready to make progress? Get in contact here.