Super vs mortgage: where should my surplus go?

It’s one of the most common questions we get asked as financial planners:

Should I put my extra cash into my mortgage, or top up my super?

And it’s a fair question. Both options have the potential to boost your long-term wealth — and the right answer depends entirely on your financial position, goals, and time horizon.

At Navigate Advisors, our team of financial planners work closely with clients to unpack this decision in the context of their bigger picture. Here’s how we guide the conversation.

What are you trying to achieve?

Before crunching numbers, we always start with purpose. Do you want:

- Greater peace of mind from reducing debt?

- A better retirement outcome?

- Flexibility to make lifestyle choices sooner?

- All of the above?

Your surplus income is an opportunity to make meaningful progress — but you need to define what “progress” looks like to you.

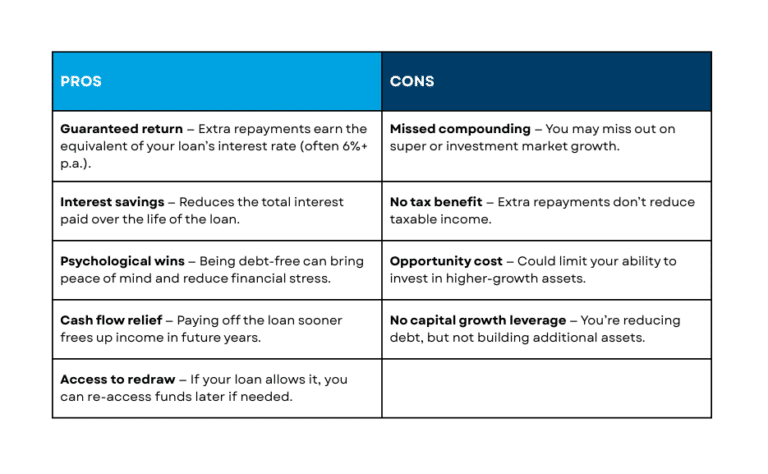

Paying down the mortgage: pros and cons

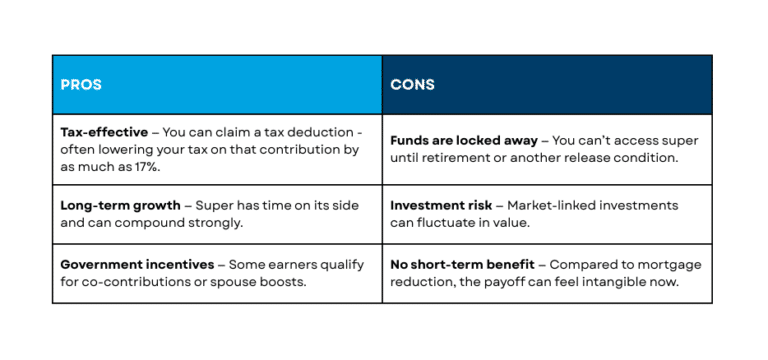

Topping up super: pros and cons

How we help clients decide

Here are some key factors we investigate with our clients:

1. Age and retirement timeline

Younger clients with time on their side may benefit from super’s compounding growth. Those close to retirement might prioritise debt-free living.

2. Tax position

If you’re in a higher tax bracket, topping up your super may reduce your taxable income and maximise tax efficiency.

3. Loan type and interest rate

With mortgage rates sitting far above historical lows, the “return” from making extra repayments can be quite compelling — especially if you’re risk-averse.

4. Cash flow flexibility

Do you need to maintain liquidity? Mortgage offset accounts can offer flexibility that super can’t match.

5. Retirement goals

A common trap we see is people focusing so hard on debt reduction that they arrive at retirement with a paid-off home but not enough super to fund their lifestyle.

So, what’s the best option?

In many cases, superannuation comes out ahead on the numbers. Your contribution benefits from an immediate tax deduction and then continues to work harder within the super environment thanks to the concessional tax rate and a long-term investment strategy that should outpace home loan interest rates.

In reality, a blended strategy often makes sense — allocating part of your surplus to super and part to your mortgage. This approach can be especially useful when:

- You’re approaching contribution caps

- Your marginal tax rate is lower

- Interest rates on your loan are particularly high

Here’s how that might look in practice:

- Salary sacrifice a small, regular amount to super

- Use the remaining surplus to pay down your loan or build your offset buffer

- Reassess each year as your income, rates, and contribution limits change

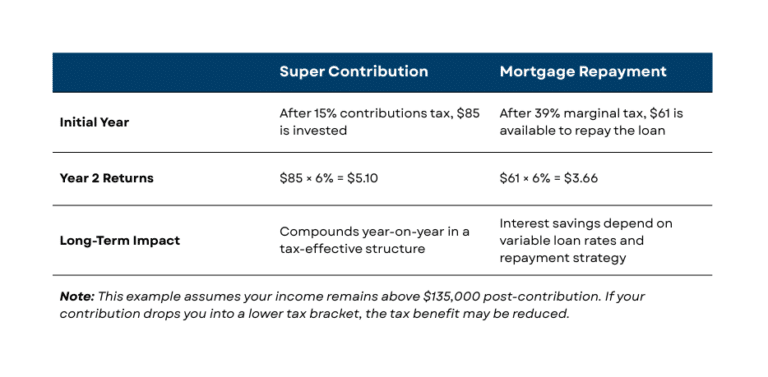

A Simple Example

Let’s say you earn over $135,000 and have $100 in surplus income:

The right choice for your surplus depends on what you value more right now — flexibility, tax savings, retirement growth, or peace of mind.

We’ve helped hundreds of locals across Wagga and the Riverina find the right balance for their situation. If you’re not sure where your surplus will have the biggest impact, let’s sit down and model it together.

There’s no one-size-fits-all answer — but there is a smart strategy that’s right for you.

General Advice Disclaimer: This article provides general information only. It does not consider your personal circumstances and should not be relied on as taxation or financial advice.