Debt Recycling: Saving, Investing, and Reducing Your Mortgage All at Once

If you’ve ever thought about how to pay off your home loan faster while building long-term wealth, debt recycling might be a strategy worth researching. It’s all about being smarter with the resources you already have—using your equity, savings, or even an unexpected windfall to both reduce your mortgage and invest for the future.

Debt recycling can sound complicated, but it’s pretty straight forward once you break it down. It’s the concept of turning your lifestyle debt into investment debt. By doing so, it helps you to increase tax-efficiency, repay your lifestyle debt faster and in most cases, start investing much sooner than you thought possible.

Conceptually, the strategy is based on the principle of debt used for investing being tax-deductible whereas debt used for lifestyle has no such benefit. Generally, lifestyle related debt includes loans for your family home, your personal car, borrowings for your holidays and even credit cards.

Let’s dive in with an example that shows how you can invest, save on interest, and still get the perks of tax-deductible debt.

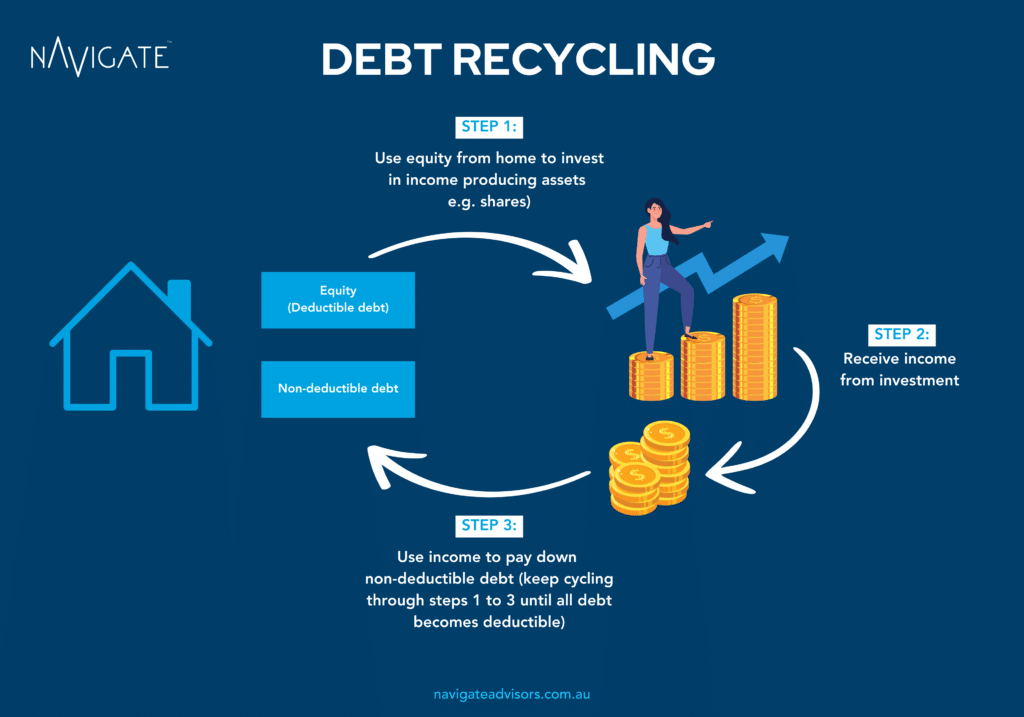

How it works?

Who is Debt Recycling Suited To?

Debt recycling isn’t for everyone. It’s best suited to those who:

- Have Stable Cash Flow: You’ll need to comfortably manage both your mortgage repayments and the investment loan.

- Want to Use Your Home Equity: If your property has built-up equity, debt recycling lets you put it to work.

- Want to Start Investing ASAP: You want to start building a share portfolio (or use managed funds) to build your wealth.

- Have Long-Term Goals: Debt recycling works best when you have the patience to let your investments grow over time to ride out ups and downs.

It’s particularly ideal for people in these scenarios:

1. You’ve got other assets already invested

If you have existing assets like a share portfolio, Employee Share Scheme or even plain old savings in your redraw/offset facility, you can turn those into a tax-deductible investment loan following the same principle as above – allowing you to invest using tax-deductible debt.

2. You’ve received a lump sum of money

Traditionally people pay a lump sum off the home loan and leave it at that. You can be much more efficient by using that additional equity to invest via a debt recycling strategy. You “split” your loan to reflect the reduced home loan amount after the lump sum as Loan 1 and then set up a second loan for the lump sum amount. That means your debt limit is the same as it was prior to receiving the lump sum but that you can now access that equity separately via drawing down on Loan 2.

3. You’re sitting on substantial equity

If your property has appreciated significantly, you might find yourself with untapped equity. By refinancing to access that equity, you can borrow to invest while ensuring the investment loan remains separate (and tax-deductible).

The Offset Account Advantage

Picture this:

- You’ve got a $400,000 home loan.

- You’ve also been saving like a champ and have $100,000 tucked away in your offset account.

Now, because of your offset account, the interest on your mortgage is only charged on $300,000 instead of the full $400,000. You’re already ahead!

What if you could use your equity to invest without it costing you extra on your mortgage repayments?

That’s where debt recycling comes into play.

How It Works: The Game Plan ($100,000 Example)

Step 1: Create Usable Equity

Build equity in your home through one of the following methods:

- Use your savings: Apply $100,000 from your savings to your home loan while keeping a cash reserve in your offset account for emergencies.

- Sell other assets: Sell assets to pay $100,000 off your home loan, but consider any capital gains tax—seek advice!

- Make extra repayments: Gradually increase repayments to build equity over time.

Alternatively, you might already have sufficient equity if your home’s value has increased, or you’ve significantly paid down your loan.

Step 2: Use Your Equity

- Reduce your home loan limit by $100,000 and continue repaying it as usual on the smaller loan.

- Use the freed-up cash flow to service a $100,000 investment loan.

- Assume the investment loan generates $6,000 in annual interest, with a potential tax saving of $2,340 if you’re in the 39% tax bracket (including the Medicare levy).

Step 3: Invest and Reap Returns

- Invest the $100,000 into a portfolio that offers tax-effective income and capital growth.

- With a 5% annual return, you could earn $5,000, translating to $3,150 in after-tax cash flow.

Step 4: Leverage the Cash Flow

Use the investment cash flow ($3,150) and your tax savings ($2,340) to pay off your home loan faster.

Step 5: Rinse & Repeat

Repeat the process until your home loan is fully repaid:

- Reduce your home loan limit.

- Increase your investment loan limit.

- Reinvest the loan proceeds.

How Does It All Look In The End?

Once your home loan is repaid, you have options:

- Sell the investments: Repay the investment loan and fund your financial goals.

- Build wealth: Redirect surplus cash flow to investments or superannuation.

- Alternative uses: Skip the “Rinse & Repeat” and use extra repayments for lifestyle goals, such as holidays or vehicle upgrades.

Why This Works:

Debt recycling is so powerful:

- You unlock tax savings

- You free up cash flow

- You start investing sooner

- You maintain financial flexibility

Debt recycling is like having your money do two jobs at once. But before you dive in, it’s important to make sure this strategy suits your financial situation. You need a steady cash flow, a good grasp of the risks, and clear loan structuring to keep things tax-deductible.

If you’re ready to put your money to work get in touch here.